Hyman Minsky in Colombia, November 1987https://t.co/QLc4pebEPt

— 地域通貨花子1 (@TiikituukaHana) October 13, 2022

7:33~

《No reason no problem in explaining it. I mean, it's not difficult. Because Ponzi finances when you borrow to pay interest. 》 pic.twitter.com/tUraIsGwTL

The assets and liabilities each are cash flows. The assets will generate profits what? The liability structure is a prior commitment of expected future incomes.

take a look at someone who is purchased the house by a mortgage. here then you have a unit that can safely cover. the interest in the principle on debt the payment commitments on liabilities by expecting income.

in this case expected wage income. such a unit will be a hedge unit. So you have rolling over Finance rolling over which I call speculative.

then there's a third thing with digital label that got me in trouble, which I called Ponzi Finance.

Ponzi finances when you borrow to pay interest.

now let us State the financial instability hypothesis. The economy is doing well. And liability structures are predominantly hedged. and this continues Until the margin is eaten up. You develop Financial structures. Where any drop and income or arising interest rates will transform some firms to Ponzi financing? When there are firms that are Ponzi financing. bankruptcies will occur bankruptcies will affect the liquidity preference of lenders and borrowers, right? Which will draw in? the external financing margin and an economy Where the prime generator of profits as business investment or housing financing? To collapses there are agents who manage portfolios who have to have risk and uncertainty valuations the risk and uncertainty evaluations are unfortunately myopic and regard to the Past. And imperfect with regard to the Future. And therefore a capitalist economy. Is subject to booms and busts?

Finish.

資産と負債のそれぞれはキャッシュフローです。資産は利益を生み出します。負債は、将来見込まれる収入をあらかじめ約束するものです。

例えば,住宅ローンを組んで家を購入した人 の場合,負債の元本の利息と負債の支払いの約 束を期待収入で安全にカバー(ヘッジ)できる単位がここにある。

さて、ローリング・オーバー 金融のローリング・オーバーを私は投機的と呼んでいます。

そして、デジタル・レーベルの3つ目の問題は、私がポンジ・ファイナンスと呼んでいるもので、問題になったものです。 ポンジ・ファイナンスとは、金利を払うために借金をすることです。

では、金融不安仮説を述べてみましょう。経済はうまくいっている。そして、負債構造はヘッジが主流である。これはマージンがなくなるまで続きます。金融構造を開発するのです。どんな低下や収入や金利の発生があっても、一部の企業はねずみ講的な資金調達に変貌します。ポンジファイナンスになっている企業があると、倒産が起こる。倒産すると、貸し手と借り手の流動性選好に影響が出ます。

外部資金余力と経済 企業投資や住宅融資など、利益の素となるものはどこか?このように、リスクと不確実性の評価は、残念ながら近視眼的であり、過去に関して不完全である。そして、将来に関して不完全。従って資本主義経済は 好景気と不景気の影響を受けます。

終了。

| #MMTp In Under A Minute (@in_mmt) |

“What the liability structure is, is a prior commitment of expected future incomes”. - Minsky When you’re the currency issuer, there is zero reliance on having an income to meet your commitments & any so called liability you issue can easily be met, on time, every time. #auspol pic.twitter.com/n1yTqY7Kfm | |

https://twitter.com/in_mmt/status/1266962958573166593?s=21

https://youtu.be/ej37UMbNv3c

https://youtu.be/NEWHMJrQj1s

Minsky talks about the financial instability hypothesis 1987

— 地域通貨花子1 (@TiikituukaHana) June 1, 2020

Hyman Minsky in Colombia, November 1987https://t.co/tBtntspU3Fhttps://t.co/FyD9a74JJM pic.twitter.com/R2iv5U9vuD

Now let us state the financial instability hypothesis quickly.

it is that in normal functioning of an economy the interest rate structure.

When the economy is doing well and liability structures are predominantly hedged.

The interest rate structure is such.

That there is a it's cheaper to finance short term than long term.

And those who can make the arrangements for financing and refinancing will shift their liability structure.

And this continues until the margin is eaten up which means higher short-term rates relative to Long rates.

short moves up relative to log.

The long rate being the market determined rate really?

And then if you have Rising interest rates.

Short-term Finance euphoric or good expectations in the economy.

You develop Financial structures where any drop in income or rise in interest rates will transform some firms to Ponzi financing.

When there are firms that are Ponzi financing.

bankruptcies will occur.

bankruptcies will affect the liquidity preference of lenders and borrowers, right?

Which will draw in?

the external financing margin and an economy

Where the prime generator of profits is business investment?

Or household or housing financing?

the collapses.

So it's an endogenous process based upon

how?

financial markets behave and how profit-seeking portfolio managers and bankers behave and businessmen behave.

There are agents operating for profits.

There are agents.

Who manage portfolios who have to have risk and uncertainty valuations the risk and uncertainty valuations are unfortunately myopic in regard to the past and imperfect with regard to the Future.

And therefore a capitalist economy.

Is subject to booms and busts?

Finish.

では金融不安定化仮説を手短に述べます。

それは、経済が正常に機能しているとき、金利構造が経済がうまくいっているときには、

負債構造はヘッジが優勢である。

金利構造はそのようなものである。

長期より短期の方が資金調達が安くなることがある。

そして、融資や借り換えの手配ができる人は、負債構造をシフトさせる。

そしてこれはマージンが食い尽くされるまで続き、それは長期金利に対して短期金利が高くなることを意味する。

短期金利は長期金利に対して上昇する。

長期金利は市場で決定される。

そして、もしあなたが上昇金利を持っているならば、

短期金融は、経済の幸福感に満ち良い期待をする。

所得の低下や金利の上昇は、いくつかの企業がネズミ講金融に変換されます金融構造を開発します。

ネズミ講的な金融をする企業があると、倒産が発生する。

倒産すると、貸し手と借り手の流動性選好に影響が出ますよね?

どちらが資金を引き寄せるか?外部資金余力と経済だ。

利益の素が企業投資であるところだ。

もしくは家計や住宅金融が崩壊する。

つまり、それは内生的なプロセスに基づくものである。

どのように?

金融市場がどう動くか、利益を追求するポートフォリオ・マネジャーや銀行家がどう動くか、ビジネスマンがどう動くかに基づいています。

利益を求めて活動するエージェントが存在する。

そしてリスクと不確実性の評価を持っているポートフォリオを管理する人 リスクと不確実性の評価は、残念ながら、過去に関しては近視眼的であり、未来に関しては不完全である。

したがって、資本主義経済は好景気と不景気の影響を受ける。

以上。

では金融不安定化仮説を手短に述べます。

それは、経済が正常に機能しているときには、金利構造が

経済がうまくいっているとき、負債構造はヘッジが優勢である。

金利構造はそのようなものである。

長期より短期の方が資金調達が安くなることがあること。

そして、融資や借り換えの手配ができる人は、負債構造をシフトさせる。

そして、これはマージンが食い尽くされるまで続く。

つまり、長期金利に対して短期金利が高くなる。

短期が長期より高くなる

長期金利は市場で決定されたレートであるということである。

そして、Rising interest rates.

短期金融は景気に陶酔したり、良い期待をしている。

所得の低下や金利の上昇が一部の企業をネズミ講的な金融に変えてしまうような金融構造が出来上がってしまうのです。

ネズミ講的な金融をする企業があると倒産が発生する。

倒産すると、貸し手と借り手の流動性選好に影響が出ますよね?

どちらが資金を引き寄せるか?

外部資金余力と経済

利益の素が企業投資であるところ?

それとも家計や住宅資金

が崩壊する

に基づく内生的なプロセスなんですね。

どのように?

金融市場がどう動くか、利益を追求するポートフォリオ・マネージャーや銀行家がどう動くか、ビジネスマンがどう動くかに基づいています。

利益を求めて活動するエージェントが存在するのです。

そしてリスクと不確実性の評価を持っているポートフォリオを管理する人、

リスクと不確実性の評価は、残念ながら、過去に関しては近視眼的であり、未来に関しては不完全である。

したがって、資本主義経済は好景気と不景気の影響を受けるのです。

以上。

:Minsky1986(邦訳『金融不安定性の経済学』),#8,231頁

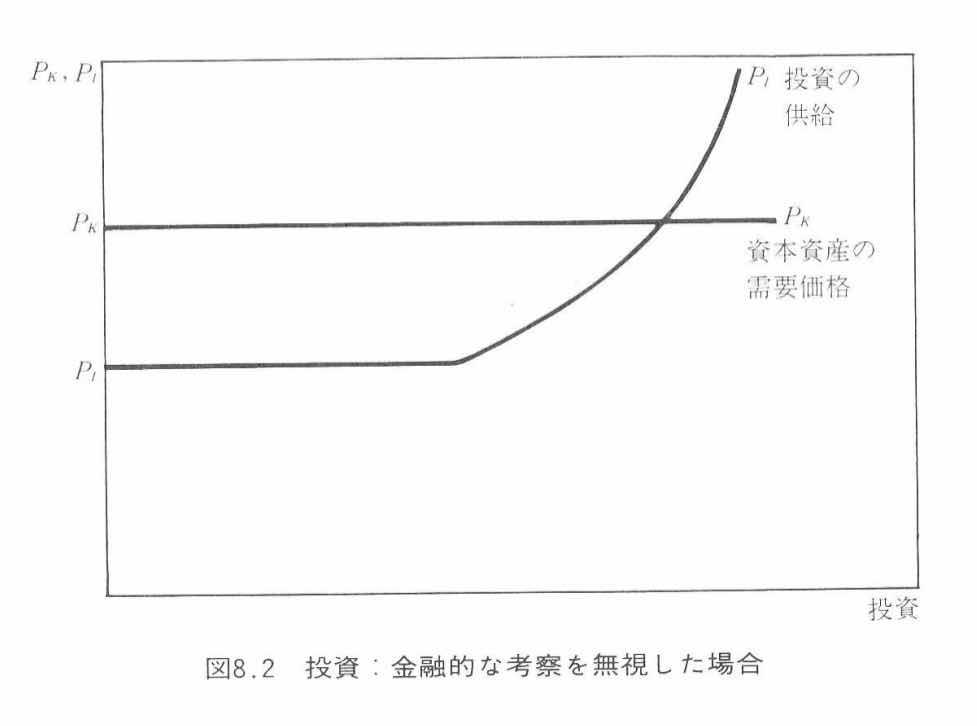

よる資金調達の増加を反映して,資本資産の需要価格を引き下げることにより,

負債取引契約を履行できなくなる危険性の増大を防ぐための安全性のゆとり幅

を増加させることができる.資金の借り手のリスクは,資本資産の需要価格が

右下がりになることにあらわれる12).それは,いかなる金融価格の中にも反映さ

れるものではない,つまりそれは,危険を埋め合わせる潜在的な収獲が存在す

る場合にのみ,債務不履行の危険の増加に身をさらしても価値がある, という

MINSKY'S ANALYSIS OF FINANCIAL CAPITALISM

by

Dimitri B. Papadimitriou

and

L. Randall Wray

The Jerome Levy Economics Institute July 1999

http://www.levyinstitute.org/pubs/wp/275.pdf25.3 Minsky's investment decisions

価格

PkI______。 。貸し手のリスク

I 。。

l 。。

Psl______。 。借り手のリスク

l______________________

Ii I* 投資

:408

しかし,短期利子率と長期利子率の上昇は,資本資産の需要価格と投資の供給価格に対して正反対の方向に影響を及ぼす。長期利子率が増加するにつれて,資本資産の需要価格は下落し,短期利子率が上昇するにつれて,投資用の産出物の供給価格は上昇する。このことにより,投資需要を誘発する価格差が縮まる傾向をもつ。もし,利子率の上昇が極端であれば,資本資産としての投資財 の現在価値が,経常産出物としての投資財の供給価格を下回ることがありうる。もし, そのような現在価値の逆転が起これば,投資活動がイ亭上に追い込まれる であろう.も し,利子率の上昇が急、激であり,投資計画の収益性にかんする評 価の下落をともなえば,現在進行中の投資計画さえ放棄されるであろう。

現r■ 価イ直の逆転ιま実際に生じることがあるが-1930年 十ににはr窪かにそ′′t が生 したし, 1974-75年 と1981-82年 には, もっとはるか|こ 限定されノこ範囲内 で丼、たたび生じた一― 投資活動の循環的な収縮および拡張は,このような極端 な場合に依存することなく生じる。投資の循環的な変動が生じるためには,資 本資産価格と金融費用を含む投資の供給価格の間の差額が,利子率の変化と逆 の方向へ変化するだけで十分である。短期および長期の利子率が低い状況の下 では,二種類の価格の間の開きが大きくなり,そのことによって内部金融に対 するクト音6金属1の上ビ率の_L昇がもたらさ才tるであろう。このことは, 投資と利潤 の上昇をもたらし,資本資産ポジションを負債によって調達する意欲の増加を

もたらす。かくして,金融市場が投資決定メカニズムの一部を担っているよう な経済はみな,強い不安定化をもたらす内在的な相互作用を抱えている。

金融的な諸条件の影響の結果,投資と利子率の間の関係は,右下がりの関数 で表現することができる。経済の動きとともに貸し手と借り手の受容可能なり スクが変化する様式と,投資が利潤を決定し,かくして,外部金融の度合を決 定する様式のゆえに,債務に体化されている取引契約の覆行の経験を反映して, 右下がりの勾配をもつ投資と利子率の関係がシフトする.右ドがりの投資と利 子率の関係は,資本資産の技術的な生産性の逓減と投資財の供給価格から引き|11される単純な系論などではない.むしろ,それは,技術的,市場的,金融的な行動を要約している。 金融的な感化力は, 不確実1生という項目のもとに一括される諸考察によつて影待されるので,投資と利子率の間の右下がりの勾配をもつ関数が議論において使用されるならば,経済のたどる径路が将来事象にかんする現在の見解を変化させるにつれて, この関数がシフトする, ということを認識すべきである。

:240

And liability structures are predominantly hedge the interest rate.

Structure is such that there is a it's cheaper to finance short term than long term.

And this continues until the margin is eaten up which means higher short-term

rates relatively long rates short moves

up relatively long the long rate being the market determined rate really.

When there are firms that are Ponzi financing bankruptcies will occur bankruptcies will affect the liquidity

preference of lenders and borrowers right which will draw in the external financing margin.

seeking portfolio managers and bankers behave and businessmen behave.

There are agents operating for profits.

それは、経済が正常に機能している時には

経済がうまくいっているときの金利構造。

そして、負債構造は、主に金利をヘッジするために

長期よりも短期の方が安く融資できるような構造になっている。

そして、資金調達や借り換えの手配ができる人は、負債構造をシフトさせる。

そして、これは証拠金が食い尽くされるまで続きます。

レート 相対的に長いレート 短い動き

市場が本当に決定されたレートであることが比較的長いレートをアップします。

そして、あなたは経済の上昇金利短期金融陶酔や良い期待を持っている場合。

あなたは、所得や金利上昇の任意のドロップがネズミ講融資にいくつかの企業を変換する金融構造を開発しています。

ネズミ講融資倒産が発生するであろう企業がある場合、倒産は流動性に影響を与えます。

貸し手と借り手の選好権(これは描画されます)の外部資金調達マージンで。

そして、利益の主要な発生源が、企業投資や家計の火事や住宅資金調達である経済では、崩壊します。

だからそれは、金融市場がどのように振る舞うか、どのように利益に基づいて内生的なプロセスです。

ポートフォリオマネージャーと銀行家の行動とビジネスマンの行動を求めて

利益のために活動するエージェントがいる。

ポートフォリオを管理するエージェントの中には、リスクを持たなければならない

と不確実性の評価は、残念ながら近視眼的なものです。

過去に関しては過去、未来に関しては不完全です。

そのため資本主義経済は好況と破綻に見舞われるのです。

終わりにします。

Now the last point that I really want to take up.

Take a look at someone who has purchased a house by a mortgage here.

If that is the situation then you have a unit they can safely cover the interest in the principle on debt.

Such a unit will be a hedge unit.

My language it'll be a unit that can fully validate its debts out of current income with a margin of safety and all that.

States was.

It means it includes both the payment of interest and the payment of principal.

Did that get true the noise or should I repeat it.

over years.

Sometimes it's formalized.

And every month every bank is given a January February March and during that bunch you will not be in debt to that bank.

up like the the next one right.

That's finishing its year right to the bank

And therefore you can keep million dollars in my example of short-term debt

forever as long as you're able to pay the interest on the debt.

with you from time to time.

into trouble with their debtors.

They can finance a hundred billion dollar debt Brazil almost did one step outside debt would it exports right .

earnings and if you committed a hundred.

And twenty percent of your net export earnings ain't going to do it.

So when interest rates go up and down the position of these countries become

sometimes speculative sometimes finance Ponzi never hedge.

to their stockholders and they pay interest to their own debtors.

any any anything like income from it.

Well Ponzi finance it means that your debt is growing in a very inefficient way.

getting time to the next crisis in this type of structuring.

So Ponzi financing will occur when a debt burden short-term debt mainly but

also long-term that is confronted with a drop in profits.

And what happens to Ponzi finance is that it both leads to cutting off areas from being externally financed.

One is the cashflow margin and the other is the equity margin.

And when the stock market collapses.

The equity margin of organizations can disappear even though to cash flow margin remains

Because it's the excess of their total value of assets over their death as the market values it.

And liability structures are predominantly hedge the interest rate.

Structure is such that there is a it's cheaper to finance short term than long term.

And this continues until the margin is eaten up which means higher short-term

rates relatively long rates short moves

up relatively long the long rate being the market determined rate really.

When there are firms that are Ponzi financing bankruptcies will occur bankruptcies will affect the liquidity

preference of lenders and borrowers right which will draw in the external financing margin.

seeking portfolio managers and bankers behave and businessmen behave.

There are agents operating for profits.

今、私が本当に取り上げたい最後のポイントです。

ここで住宅ローンで家を購入した人を見てみましょう。

それが状況なら、あなたは彼らが安全に債務の原則への関心をカバーできるユニットを持っています。

そのようなユニットはヘッジユニットになります。

私の言葉は、現在の収入からの借金を安全なマージンで十分に検証できるユニットになるでしょう。

であったときにすべてのビジネスで確実にヘッジファイナンスを行う場合。

それは利子の支払いと元本の支払いの両方を含むことを意味します。

それは本当のノイズになるか、それとも繰り返すべきか。

何年にもわたって粗利を稼ぐことを学ぶプロジェクトがあるとしましょう。

時々それは形式化されています。

そして毎月、すべての銀行に1月、2月、3月が与えられ、その間、その銀行に対して借金をすることはありません。

ように混同されているかもしれません。

それは銀行にとって正にその年を終えている

したがって

、借金の利息を支払うことができる限り、私の短期借入金の例では、何百万ドルも永遠に維持できます。

時々彼らがあなたに対処する用意があるかどうかに影響を与えていることに気付くかもしれません。

が債務者とトラブルに陥るたびに行っていることです。

彼らは1000億ドルの借金を賄うことができますブラジルはそれが輸出する場合、借金の外に一歩近づきました。

収益の事前のコミットメントであり、100をコミットした場合です。

そして、あなたの純輸出収入の20パーセントはそれをするつもりはありません。

したがって、金利が上下するとき、これらの国の位置は

時々投機的になり、時々ポンジは決してヘッジしません。

彼らは株主に配当を支払い、自分の債務者に利息を支払います。

それから収入のような何も決して得なかった本に彼らが書いたちょうど収入に基づいて。

まあポンジーはそれはあなたの借金が非常に非効率的な方法で成長していることを意味します。

、このタイプの構造化で次の危機への時間を得るだけです。

したがって、ポンジ融資は、負債が主に短期債務を負担するときに発生しますが、

長期的には利益の低下に直面します。

そして、Ponziファイナンスに何が起こるかは、それが両方とも外部からのファイナンスを受けることから領域を切り離すことにつながるということです。

1つはキャッシュフローマージンで、もう1つは株式マージンです。

そして、株式市場が崩壊したとき。

キャッシュフローマージンが残っていても、組織の株式マージンは消える

それは、市場がそれを評価するとき、それは彼らの死を超える資産の彼らの総価値の超過だからです。

そして、負債構造は主に金利をヘッジしています。

長期的な資金調達よりも短期的な資金調達の方が安いという構造があります。

そして、これはマージンが食い尽くされるまで続きます。つまり、より高い短期

レートが比較的長く、ショートレートが比較的長く上昇し

、ロングレートが実際に市場が決定するレートです。

Ponzi融資の破産が発生している企業がある場合、破産は

、外部の融資マージンを引き込む貸し手と借り手の権利の流動性選好に影響を与えます。

追求型のポートフォリオマネージャーや銀行家の振る舞い、ビジネスマンの振る舞いに基づく内生的なプロセスです。

営利目的で営業しているエージェントがいます。

「…経済の具合がよい期間が長くなると、会社の重役室では、二つのことがはっきり

その結果、穏やかな成長の時期は、期待の増大をもたらす。そしてレバレッジ

よる資金調達の増加を反映して,資本資産の需要価格を引き下げることにより,

負債取引契約を履行できなくなる危険性の増大を防ぐための安全性のゆとり幅

を増加させることができる.資金の借り手のリスクは,資本資産の需要価格が

右下がりになることにあらわれる12).それは,いかなる金融価格の中にも反映さ

れるものではない,つまりそれは,危険を埋め合わせる潜在的な収獲が存在す

る場合にのみ,債務不履行の危険の増加に身をさらしても価値がある, という

見解を映し出しているのである.》

《 内部的なキャッシュ·フローは, (個別企業にとっても,経済全体にとっても)

ある水準の投資の資金を支払うことを可能にする,内部的なキャッシュ·フロー

あるいは準地代QNは,投資財の価格PIおよび産出量I1と,P1I1 = QNという公式

によって結びついているので,ひとたび内部的な期待キャッシュ·フロー(Q)に

見積もられると, それらと投資の間の関係は,直角双曲線(図8.3のQNQN)

よって表わされる。この直角双曲線と投資用の産出物の供給価格P1の交点は、

予想内部資金によって金融できる投資量I1 (内部的)をもたらす(図8.30のA点

参照)。》《ミンスキーが主張したように(そして私の簡単なマクロ経済モデルが証

明したように)、仮にすべての投資の目的が生産のためであったにしても、危機は起こり得る。と

いうのは、金融システムは、「投資意欲を加速させる信号を発生し、加速する投資にたいし金融を

つけることが可能だ」(Minsky, 1969, p.224)からだ。ブームと破綻は資本主義の特性に他ならない。だ

から、民間負債の対GDP比の上昇傾向が予想できるのだ。一九四五年からアメリカの民間負債が

金融システムを改善したにも拘わらず、伸び続けてきたのがその例になる。これに対処する唯一の

方法は、現在インフレや失業率がそうであるように、民間負債の対GDP比を経済運営における重

要事項に指定し、そしてマクロ経済の統御の道具として、国家がマネーを創出する権能を行使する

ことだ。とりわけ、民間負債が危険なレベルへと近づき始めたとき、つまり、まだ対GDP比が1

00%よりもかなり低く、つまり、手綱が効かなくなった金融によってもたらされた現在のレベル

よりもまだはるかに低い時点で、国家のマネー創出権を行使することだ。》キーン『次なる金融危機』113頁ミンスキーは危機を警告しただけではなくコミュニティバンクの創設も提案している。《ささやかに見える提言もあった。そのひとつが、一九九二年に彼が中心となってまとめた提言「コミュニティ・デベロップメント・バンクス(18)」である。コミュニティ・デベロップメント・バンク(CDB)とは、名前のとおり地域社会の発展を目的とする銀行のことで、アメリカでは商業銀行の一種とされ、財務省の一部局であるコミュニティ・デベロップメント・バンク・インスティテューション・ファンドの管轄とされている。

ミンスキーたちはこのCDBに理論的基礎を与えるとともに、さらに強化するための制度的提案をしている。

…

「CDBの中心的な目標は、従来の銀行が十分にサービスを展開していない地域に貸出と支払を行い、規模が小さすぎるために投資銀行や商業銀行の関心をひかない限定地域のビジネスに融資することである(20)」》

(18)Hyman Minsky, Dimitri Papadimitriou, Ronnie Phillips, L. Randall Wray, “Community Development Banks,” The Jerome Levy Economics Institute, Working Paper No. 83, Dec. 1992.(20)Ibid.

経済学者の栄光と敗北 ケインズからクルーグマンまで14人の物語

平成25年7月25日 東谷暁 #6よりMitchell2019

25.3 Minsky's investment decisions

価格

PkI______。 。貸し手のリスク

I 。。

l 。。

Psl______。 。借り手のリスク

l______________________

Ii I* 投資

:408

ハイマン ・ミンスキ ー

「金融不安定性仮説 」とは 、次の二つの定理から成る 。金融不安定性仮説の第一定理は 、経済には 、安定的な枠組みと不安定な枠組みとがあるというものである 。そして 、金融不安定性仮説の第二定理は 、繁栄が続くと 、経済は安定をもたらす金融関係から 、不安定化に向かう金融関係へと移行するというものである ★ 5 。

★ 5 H y m a n P . M i n s k y , ' T h e F i n a n c i a l I n s t a b i l i t y H y p o t h e s i s , ' W o r k i n g P a p e r N o . 7 4 , T h e J e r o m e L e v y E c o n o m i c s I n s t i t u t e o f B a r d C o l l e g e , 1 9 9 2 , p . 8 .

富国と強兵ハイマン ・ミンスキ ーもまた 、亜流ケインズ派を批判して 「不確実性のないケインズなど 、王子のいないハムレットのようなもの 」と嘆いている ★ 4 。

★ 4 H y m a n P . M i n s k y , J o h n M a y n a r d K e y n e s , M c G r a w H i l l , 2 0 0 8 , p . 5 5 .

富国と強兵ミンスキーの金融不安定性仮説 - ミンスキーの金融不安定性仮説とはど... - Yahoo!知恵袋https://detail.chiebukuro.yahoo.co.jp/qa/question_detail/q1443896734ベストアンサーに選ばれた回答

経済主体が、利益目的で資産を購入するとき、

借入をすることがある。

しかし、資産を購入しても、

その資産からのキャッシュフローにより、

借入の返済が賄えている間は、それほど問題はない。

というより、これは資本主義の普通の活動。

景気が良くなるにつれて、

資産から得られるキャッシュフロー自体よりも、

資産自体が値上がりすることによる

将来のキャッシュフローを当て込んで、

資産が取引されるようになる。(投機的取引)

この取引のための、資金が、短期貸付で行われるようになってくると、

貨幣供給量は中央銀行の制御が

難しくなる。(主流派経済学と違って、貨幣供給量は

取引によって生み出されるのであり、逆ではない)

こうなってくると、社会全体が「金融的多幸症」

といわれる状況を呈するようになる。

資産の価格自体が、取引を促進し、それにより

短期貸付が増加し、それにより、資金供給が増えて、

社会全体の雰囲気が「多幸症」的になること。

取引が活発化すれば、景気が良くなる、というのは主流派経済学と同じだが、

ミンスキーの場合、取引自体が短期貸付を通じて

景気を向上させる資源となる資金を供給し、それがふたたび

景気を刺激し、資産価格を引き上げることになる。

この点は、資金供給を一定(外生変数)としたうえで、取引が増えれば、物価・金利が

上昇するという主流派経済学の考え方とは、まったく違っている。

だから、主流派のように、金利・物価が上昇することにより、

マーケットメカニズムを通じて、自然と均衡状態に戻ってゆく経路は

想定されていない。というより、

「複雑に金融が絡み合う現代資本主義においては」(これ、ミンスキーの

枕ことば)、マーケットには、

均衡を破壊するメカニズムが内在しているのであり、

均衡を導く機能はない。

で、資産価格上昇・金融的多幸症の発展の中で、

資産を購入した際に発生した借り入れの返済や支払いを

資産からのキャッシュフローだけでは賄うことができず、

資産の価値が将来上昇するという期待だけを根拠に

再借り入れすることができる可能性にのみ依存して

短期借り入れを繰り返す企業が急増する。こうした

企業の資金調達の在り方を「ポンツイ金融」と呼ぶ。

当然のことながら、こうしたことが可能なのは、

借入れ増加による金利支払いの増加が

資産の価格上昇予想によって支えられる間のこと。

他方で、貨幣供給量の急増とインフレ率の

急上昇に中央銀行が危機感を持てば、

中央銀行は政策金利を引き上げざるを得ない。

ほんのわずかな金利引き上げであっても、

ポンツイ金融の状況にある企業は

短期資金の調達が一気に困難化し、

破産が急増し、資産市場が一気に崩れる。

そうなると、ポンツイ金融に至る前の状況(とりあえず、

投機的的金融状況と呼ぶが)にあった企業が

資産価格の急落に伴い、次から次と、ポンツイ金融化し、

連鎖的に破たんする。

こうなったときに、中央銀行にできることは、

企業間の支払い困難の連鎖を最小にするため、

銀行に対する引き出し要求に応じられるように

市中銀行に資金を供給し続けること(レンダー・

オブ・ラストリゾート政策)だけであるが、

その結果、不況下の持続的物価上昇である

スダグフレーションが発生する。

というわけで、

・ポンツイ金融

・金融的多幸症

・短期貸付・借入による資産売買の取引

・内生的貨幣供給(要するに、貨幣は取引により生まれるのであって、

中央銀行などによって、外生的に決められるわけではない)

・レンダー・オブ・ラストリゾート政策

・「複雑に金融が絡み合う現代社会においては」

といった言葉・表現が用いられていれば、

テスト的には、一定の点数が取れるか、と。(経済学、リンク::::::::::)

Minsky by Keen

http://nam-students.blogspot.com/2020/04/minsky-by-keen.html

キーン2018^2017

https://nam-students.blogspot.com/2019/04/can-we-avoid-another-financial-crisis.htmlCrash Course on Hyman Minsky, L. Randall Wrayレイはミンスキーの弟子。ミンスキーを論じた著書もある。

https://www.amazon.co.jp/Why-Minsky-Matters-Introduction-Economist-ebook/dp/B00XNZA8COミンスキー,金融不安で見直される経済学者 CAN “IT” HAPPEN AGAIN? +テイラールール

11:55

返信削除ここで、金融不安定仮説を簡単に述べておこう。

それは、経済が正常に機能している時には

経済がうまくいっているときの金利構造。

そして、負債構造は、主に金利をヘッジするために

長期よりも短期の方が安く融資できるような構造になっている。

そして、資金調達や借り換えの手配ができる人は、負債構造をシフトさせる。

そして、これは証拠金が食い尽くされるまで続きます。

レート 相対的に長いレート 短い動き

市場が本当に決定されたレートであることが比較的長いレートをアップします。

そして、あなたは経済の上昇金利短期金融陶酔や良い期待を持っている場合。

あなたは、所得や金利上昇の任意のドロップがネズミ講融資にいくつかの企業を変換する金融構造を開発しています。

ネズミ講融資倒産が発生するであろう企業がある場合、倒産は流動性に影響を与えます。

貸し手と借り手の選好権(これは描画されます)の外部資金調達マージンで。

そして、利益の主要な発生源が、企業投資や家計の火事や住宅資金調達である経済では、崩壊します。

だからそれは、金融市場がどのように振る舞うか、どのように利益に基づいて内生的なプロセスです。

ポートフォリオマネージャーと銀行家の行動とビジネスマンの行動を求めて

利益のために活動するエージェントがいる。

ポートフォリオを管理するエージェントの中には、リスクを持たなければならない

と不確実性の評価は、残念ながら近視眼的なものです。

過去に関しては過去、未来に関しては不完全です。

そのため資本主義経済は好況と破綻に見舞われるのです。

終わりにします。

You develop financial structures where any drop in income or rising interest rates will transform some firms to Ponzi financing.

返信削除When there are firms that are Ponzi financing bankruptcies will occur bankruptcies will affect the liquidity

preference of lenders and borrowers right (which will draw in) the external financing margin.

返信削除あなたは、所得の任意の低下や金利の上昇は、ねずみ講融資にいくつかの企業が変換されます金融構造を開発しています。

ネズミ講の融資倒産が発生するであろう企業がある場合、倒産は流動性に影響を与えます。

貸し手と借り手の権利の優先順位(これは、外部資金調達マージンを描画します)。

返信削除You develop financial structures where any drop in income or rising interest rates will transform some firms to Ponzi financing when there are firms that are Ponzi financing bankruptcies will occur

bankruptcies will affect the liquidity preference of lenders and borrowers right (which will draw) in the external financing margin.

あなたは、所得や金利の上昇の任意のドロップは、倒産が発生します

ねずみ講融資倒産である企業があるときにねずみ講融資にいくつかの企業を変換する金融構造を開発します

倒産は、外部資金調達のマージンで貸し手と借り手の権利(これは描画されます)の流動性の優先順位に影響を与えます。

Minsky talks about the financial instability hypothesis 1987

返信削除Hyman Minsky in Colombia, November 1987

https://youtu.be/9mHBrixVarU?t=11m55s

https://twitter.com/in_mmt/status/1266962958573166593?s=21

以下はキーン『次なる金融危機』邦訳第1章より。

返信削除《…彼ら[主流派]の基本想定状態は均衡であって、危機ではなかった。どんな

「外生的ショック」であっても、そのあとでは均衡へ戻ると想定された。また

金融部門が欠けていた。そのためミンスキーは彼自身の理論を生み出さねば

ならなかった、それを彼は「金融不安定性仮説」と命名した。それによって彼は、

資本主義は「本質的に欠陥を持つ」という結論に到達した。

…

ミンスキーは「負債が資本主義経済の本質的な性質だ」(Minsky,1977b)と主張し

た。というのは、利潤を内部留保した上で、残った額を投資するように求められる

が、それには借入れが当てられるからだ…。これが資本主義に中期的な循環過程をも

たらし、それが多数回にわたって繰り返され、過大な民間負債を蓄積させる長期的

傾向をまねくのだ。

「…経済の具合がよい期間が長くなると、会社の重役室では、二つのことがはっきり

してくる。まず負債の存在が容易に正当化され、負債が重い部門が好調になる。

つまり、レバレッジ(てこの原理を使うこと。元手の何倍も借金して投資額をふ

やし、利得を大きくふくらませること)が引き合うようになる」(Minsky,1977b)

その結果、穏やかな成長の時期は、期待の増大をもたらす。そしてレバレッジ

を増大させる傾向がある。その点について、ミンスキーは、彼のもっとも有名な

文章でつぎのように述べている。「安定~つまり平穏~は、循環的過去と資本

主義的金融制度を持つ世界では、不安定に他ならない」(Minsky,1978)。

…ブームの時期の金融需要によって、資金市場の金利を上昇させ、そうでなけれ

ば実行可能だった保守的な投資を減らしてしまう。ブームの頂点で、株の過大

評価を予感して、株式市場への参加者は株を売り払う。そのため信用崩壊の

引き金が引かれる(Minsky,1982)。》

Minsky, H. P. (1977b) The Financial Instability Hypothesis: …

Minsky, H. P. (1978) The Financial Instability Hypothesis: …

Minsky, H. P. (1982) Can ‘It’ Happen Again? …

ミンスキーは(「過去三回の大規模金融危機のうち、およそ九回を予言していた」と

揶揄されるが)代替案も持っていて、1965年実質的にJGPを創案しているとされる*。

*

bill mitchell blog

http://bilbo.economicoutlook.net/blog/?p=44754

返信削除さて、ここで金融不安仮説を手短に述べておこう。

それは、経済の正常な機能において

経済がうまくいっているときの金利構造。

そして負債構造は金利をヘッジすることが主流である。

あるような構造になっています。 長期より短期の方が資金調達が安くなります。

そして融資や借り換えの手配ができる人は、負債構造をシフトしていく。

そして、これはマージンが食い尽くされるまで続き、それは短期金利の上昇を意味する。

短期金利が上昇し、相対的に長期金利が上昇し、短期金利が上昇する。

相対的に長い金利が上昇し、長い金利は市場で決定される金利になります。

そして、短期金利が上昇すると、短期金融は幸福感に包まれ、経済への期待が高まります。

収入の減少や金利の上昇によって、一部の企業がねずみ講的な金融に変化する金融構造が生まれます。

ポンジファイナンスを行う企業があると、倒産が発生し、流動性に影響を与える。

を優先させ、外部からの資金調達マージンを引き込む。

そして、利益の主な源泉が企業投資や家計の火災、住宅融資であるような経済では、破綻が起こります。

つまり、金融市場がどう動くか、利益を求めるポートフォリオ・マネージャーや銀行家がどう動くかに基づいた内生的なプロセスなのです。

金融市場がどう動くか、ポートフォリオ・マネージャーや銀行家がどう動くか、ビジネスマンがどう動くかに基づいています。

利益を追求するエージェントが存在します。

ポートフォリオを管理するエージェントがいます。

リスクと不確実性の評価は、残念ながら近視眼的なものです。

過去に関しては近視眼的であり、未来に関しては不完全である。

従って資本主義経済は好況と不況に見舞われる。

以上。

Now let us state the financial instability hypothesis quickly. It is that in normal functioning of an economy. The interest rate structure when the economy is doing well. And liability structures are predominantly hedge the interest rate. Structure is such that there is a it's cheaper to finance short term than long term. And those who can make the arrangements for financing and refinancing will shift their liability structure. And this continues until the margin is eaten up which means higher short-term rates relatively long rates short moves up relatively long the long rate being the market determined rate really. And then if you have rising interest rates short-term finance euphoric or good expectations in the economy. You develop financial structures where any drop in income or rising interest rates will transform some firms to Ponzi financing. When there are firms that are Ponzi financing bankruptcies will occur bankruptcies will affect the liquidity preference of lenders and borrowers right which will draw in the external financing margin. And in the economy where the prime generator of profits is business investment or household fire or housing financing the collapses. So it's an endogenous process based upon how financial markets behave and how profit seeking portfolio managers and bankers behave and businessmen behave. There are agents operating for profits. There are agents who manage portfolios who have to have risk and uncertainty valuations the risk and uncertainty valuations are unfortunately myopic. In regard to the past and imperfect with regard to the future. And therefore a capitalist economy is subject to booms and busts. Finish.

返信削除Now let us state the financial instability hypothesis quickly.

返信削除It is that in normal functioning of an economy.

The interest rate structure when the economy is doing well.

And liability structures are predominantly hedge.

The interest rate structure is such that there is a it's cheaper to finance short term than long term. And those who can make the arrangements for financing and refinancing will shift their liability structure. And this continues until the margin is eaten up which means higher short-term rates relatively long rates short moves up relatively long the long rate being the market determined rate really.

And then if you have rising interest rates short-term finance euphoric or good expectations in the economy.

You develop financial structures where any drop in income or rising interest rates will transform some firms to Ponzi financing.

When there are firms that are Ponzi financing bankruptcies will occur.

Bankruptcies will affect the liquidity preference of lenders and borrowers right which will draw in the external financing margin.

And in the economy where the prime generator of profits is business investment or household fire or housing financing the collapses.

So it's an endogenous process based upon how financial markets behave and how profit seeking portfolio managers and bankers behave and businessmen behave.

There are agents operating for profits. There are agents who manage portfolios who have to have risk and uncertainty valuations.

The risk and uncertainty valuations are unfortunately myopic.

In regard to the past and imperfect with regard to the future.

And therefore a capitalist economy is subject to booms and busts.

Finish.