【官僚制の真相💐】公共政策実施における予算編成過程モデルの解説:経済理論解説 2023/07/19

Introduction:マクロ経済学を修めたい💛

経済学部に通う私も

いよいよ大学「学部」最終年になり

学問に全力を注ぐ時間も限られてきました👍

「知は力なり」という言葉を信じて

残りの大学生生活を満喫したいと思います

学部レベルのマクロ経済学は

個人的によく理解できたつもりです

しかしながら、本当の経済の動向を理解するには、学部レベルの知識ではお話になりません😥

実際の経済動向や政治と結びつけながら

応用できる能力がなければ

知識を持つ意義も小さくなってしまいます💦

何事もアウトプット前提のインプットが

大事であると、noteで毎日発信してきました

これは、どのような内容で

あっても当てはまります👍

先行研究の論文を一概に読んでも

記憶に残っていなかったり

大切な観点を忘れてしまっていたりしたら

学習の進捗は滞ってしまうと思います

だからこそ、この「note」をフル活用して

自分の知識を1%でも、定着させ

誰にでもわかりやすい解説をアウトプットできるように努めていきたいと思います

私がこれからアウトプットする公共経済政策実施のための予算編成過程における官僚の行動メカニズムについての要点整理をどうぞご愛読ください📖

官僚制における公共経済政策と予算編成過程

予算編成過程では、官僚が重要な役割を果たすことになります

だからこそ、経済学を学ぶ上で、官僚のモデル分析の必要性があると私は考えています

そのため官僚制の経済分析の基本モデルを出発点として、 W.A.ニスカネンが展開したモデルについて考察していきたいと思います

官僚の役割

民主制の政治システムにおける官僚の役割について考えていくことにしましょう

具体例として、M・ウェーバーによる官僚像を取り上げます

「彼(官僚)の行う行政は、没主観的な官職義務に基づく職業労働であり、この行政の理想は、『怒りも興奮もなく』個人的動機や感情的影響の作用を受けることなく、恣意や計算不能性を排除して・・・厳に形式主義的に、合理的規則にしたがって・・・処置をするということである」

(M.ウェーバー『支配の社会学』)より、一部抜粋

ウェーバーの視点をまとめると以下のように整理できると思います📝

個人的利害関係に左右されることなく、中立かつ公正に、規律にしたがって自らに与えられた職務を忠実に果たしていく官僚像を挙げていますね

そして、政党や政治家が決定した政策を、与えられた規則・権限・予算に従って忠実に執行していくという行政の実務担当者としての役割を担っているのです

総じて、現実の政治システムでは、官僚は、たんなる実務担当者としての役割を超えて、さまざまな機能を果たすことがわかりますね📝

現実の政治システムにおける官僚の役割

ぜひ、こちらの記事から詳細はご確認くださいね

①政策の立案機能

法案作成には、政策分野に関する専門知識や情報だけでなく、それを法案として作成するための高度な法律的知識も必要となりますね

したがって、官僚は、本来、政治家の役割である政策を立案し、法案を作成する機能を果たすのです🔥

②官僚の自由裁量

成立した法律は一般的な規定でしかありません

よって、官僚には法律の現実の運用に関して、広範囲の自由裁量が与えられているのです📝

すなわち、確固とした法的根拠規定のない行政指導の実施することが求まります

したがって、官僚は事実上、自らの裁量で経済・産業界を規則することができると言えるのです👍

③予算編成機能

予算編成には、実現可能性に対する膨大な情報と経済への知識が必要であることに間違いはないはずですよね

しかし、政治家の有する情報量は限られ専門知識を有する官僚が必要になるというのです

よって、官僚主導での予算編成が実施されるというのが官僚制のもとでの経済政策分析になるのです

したがって、官僚は、自らの考えに基づいて

政策を立案し、これを裁量的に実行に移し

そのために必要な予算を獲得することができるということです

今日における経済体制は、①行政国家

②官僚主導国家、③官僚政治、という要素に

該当することが多いですから

私たちが、現実の政策形成過程を分析するには、官僚制の分析が不可欠ということを

ご理解いただけたのではないでしょうか?

そして、この投稿で取り上げるニスカネンは、官僚主導の予算編成過程を通じた公共財の供給水準の決定プロセスをモデル化したとして

経済学会に大きな功績を残しました

この功績と素晴らしい理論について

一緒に学んでいくことにしましょう

公共財供給水準の決定プロセス🌟

以下では、社会に対する公共財供給の決定プロセスについて、ニスカネン・モデルをベースに解説したいと思います

道路やダム、公園など、私たちが私費的な

費用を払わなくとも使用できる公共財は

政府が供給主体であります

その政府の中で、社会に対してどれくらいの

公共財供給量(G)を決定するのか

という議論が成されていると思います

ここの意志決定メカニズムにおいて

官僚が関わっており予算編成過程において

官僚が重要な役割を果たすことは述べてきた通りです

ニスカネン・モデルの前提条件

まずは、このモデルの前提条件や設定を確認しましょう

官僚の目的は大きく2つあるとされています

詳しくは、A.ダウンズ(1967)『官僚制の解剖』において

官僚の目的に関する詳細な研究が実施されていますので、上記の本をご参考に各自学習されてみてくださいね💖

基本的な考えとして、職員はすべて、以下における一般的な目的から生じる多様な目的をもっていると仮定されています

(1)権力(2)金銭の収入(3)威信

(4)便宜(5)安全(6)個人的忠誠

(7)作業の練達した遂行に関する自負心

(8)公共の利益に奉仕したいという希望

(9)特定施策に対する信奉

これらが目的対象としてあげられると言及されています📝

そして、最初の5つの目的は

自己利益の『純粋な』表現と解釈できますよね

なお、忠誠は対象により

部分的に自己利益になったり、ほとんどまったく利他的になったりするでしょう

練達の自負心もまた、『混合的』動機であると分類できます

そして、最後に

公共の利益に奉仕したいという希望は

ほとんど純粋に利他的であると言えます

ただ、特定施策への信奉は漠然としていることも事実なのです

したがって、職員の『効用関数』は

自己利益的目的および利他的目的の両者から

構成される、という見解に基づいて議論が進んでいくのです

官僚は、自身が担う役割と責務により

利己的な目的から利他的な目的まで多様な目的を有していると考察できますよね

このような想定の下、ニスカネンは

いずれの目的を達成するためにも、自らの所属する組織の維持・拡大が必要ということに焦点を当てました

要するに、組織の維持・拡大、施策の実現には予算を獲得する必要があるということです

何事にもお金がなければ、物事を前に進めることもできませんから

至ってシンプルな議論で素晴らしいと考えます

総じて、ニスカネン・モデルにおける官僚の

意志決定メカニズムにおける目的とは予算(Budget)の最大化ということになるのです

政治家と官僚の間に存在する情報の非対称性

予算編成にあたっては

専門的知識を有する官僚が、政治家よりも

情報に関して優位にある、という想定も

重要なポイントになります

まず、官僚は、豊富な知見と高度な情報収集能力に基づいて公共財(G)の供給面(費用情報)も需要面(国民のニーズ)も情報を完全に把握していると言うことです

その一方で、国会に出席する政治家は

選挙などを通して得られた公共財の需要面の

情報しか持たない、という点で

有する情報が相対的に少ないのです😅

したがって、より多くの情報を有する官僚が、予算編成過程において重要な役割を果たすことがわかってきたのではないでしょうか?

予算編成過程のプロセス

現実の予算編成過程は、様々なプロセスを経て編成されるので、複雑な議論が成されると思われますが、特徴は大きく2点あると思います

① 予算案の作成は、財務省を中心とする官僚が行うこと

② 政治家は、国会での審議・採決を通じて

予算の最終的決定権を有すること、であります

ここで、ニスカネンは、予算編成過程を

2段階のプロセスへと単純化しました

1:官僚による予算案の作成と議会への提出

予算案の内容については、公共財の供給量(G)とその供給に必要な予算額(B:Budget)の組合せを提示します

そして、肝心なポイントなのですが

予算案作成の第一の条件として

「予算案は実現可能なものでなければならない」ということが考えら得ますね

要するに、提示された予算額で実際にかかる

総費用(C:Cost)を賄うことができなければならないということです

したがって、私たちは、経済政策実施における制約条件「①:B≧C」を得ることになるのです

2:議会による予算案の審議・採決

そして、2段階目のプロセスとして

議会の可否の決定方法を確認しましょう

何より、政治家は、公共財の費用情報を持ちません

したがって、予算案の公共財水準を供給するのに、提示された予算額が必要かどうかの判定ができないのです

その一方で、政治家は、選挙などを通して

国民が持つ公共財の需要情報を有しているとモデルでは仮定されていましたね

したがって、予算案の公共財水準に対する国民の支払い許容額を把握できるということが政治家の意志決定メカニズムにおいて働くのです

つまり、国民の公共財に対する支払い許容額(WTP)が予算額(B)以上であれば

予算案を承認(可決)することになるのです

この結果、予算編成過程における第2の制約条件「②:WTP≧B⇒承認」を得ることができるのです

当然、国民の公共財に対する支払い許容額(WTP)が予算額(B)を下回るのではあれば

国民はその公共財に対して便益よりも費用負担が大きくなってしまうので、対価を払うことをしません

結果として、たとえその政策を実施したとしても大赤字になってしまうのです

総じて、予算編成過程における官僚の最適化行動についてまとめると、官僚は、議会で承認される予算案を作成しなければならないという制約に対峙していることになります

したがって、予算案作成の第二の条件として、制約条件「②:WTP≧B」が満たされなければならないことがご理解いただけると思います

ニスカネン・モデルにおいて官僚は、予算の最大化を目的とし、制約条件①、②をともに満たす予算案を作成することを志します

そして、以下では

予算編成過程における官僚の最適化行動に対して、ニスカネン・モデルに基づく経済理論分析を講じていきます

予算編成過程における官僚行動の定式化

官僚は、①実行可能性と②議会の承認を条件として、獲得する予算が最大になるような予算案を作成することになります

官僚は「予算の最大化」を目的として最適化行動を図ります

ただし、以下の実行可能性に対する制約を考慮していることを忘れてはなりませんね💖

① 実行可能性:B≧C

② 議会の承認:WTP≧B

需要/供給曲線の基本的知識の確認

ここで、部分均衡分析には欠かせない

一般的な需要・供給曲線についてお復習いしたいと思います📝

まず、供給曲線S(G,P)とします

これは、費用曲線を微分した結果導出される限界費用曲線:MC(G,P)に他なりません

なお、固定費用をゼロとすると、総費用は供給曲線の下側の面積で表されることになるのです

また、需要曲線D(G,P)についても確認しましょう

これは、国民の公共財から得られる便益曲線を微分することによって、導出される限界支払許容額曲線 V(G,P)になります

なお、支払許容額(WTP)は、需要曲線の下側の面積で表されることをご確認いただきたいと思います

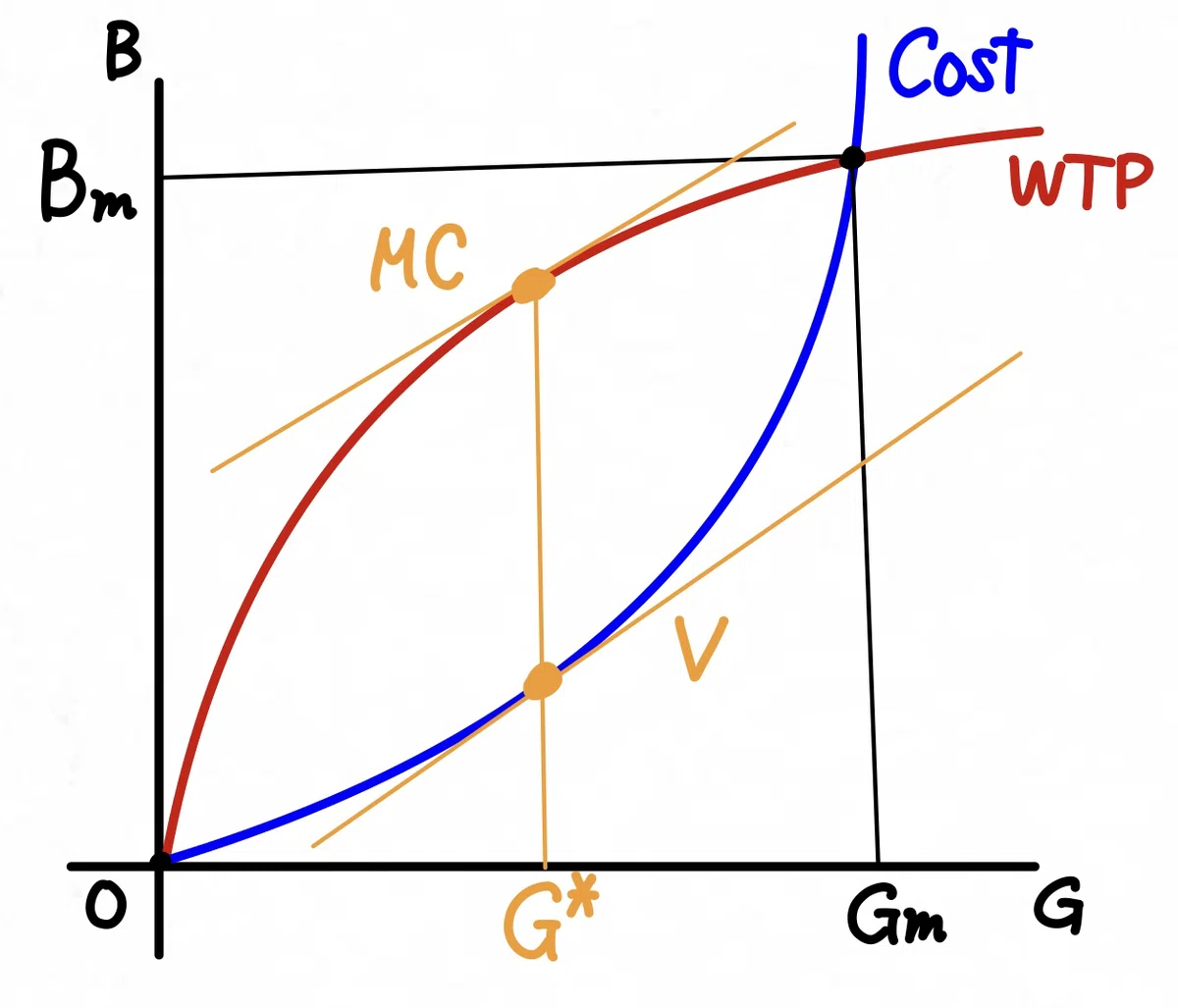

ニスカネン・モデルの実現可能性領域

ニスカネン・モデルの実現可能性領域

これは、公共財(G)の供給曲線・需要曲線に関しても同様に議論することができますので

このまま話を進めていくことにしましょう👍

官僚は、①実行可能性と②議会の承認を条件として、獲得する予算が最大になるような予算案を作成することになります

官僚は「予算の最大化」を目的として最適化行動を図ります

ただし、以下の実行可能性に対する制約

① 実行可能性:B≧C

② 議会の承認:WTP≧B

を考慮した結果、上記の図における黄色のコアが実現可能性領域として求められるのです📝

ニスカネン・モデルのインプリケーション🌟

以下では、ニスカネン・モデルの分析結果をまとめていきます

官僚は、予算の最大化を図った結果

公共財量Gmに対する予算額Bmの予算案を作成することになります

これは、縦軸に予算額(B)、横軸に公共財供給量(G)をとった図を用いて説明されます📝

ニスカネン・モデルの結論

ニスカネン・モデルの結論

この予算案Bmは、実現可能性領域にありますので、制約条件を満たします

よって、国会における議会の承認を得られ

公共財量Qmが、実際に社会に供給されることになるのです

しかし、このGmという公共財水準は本当に社会的に望ましい供給量と言えるのでしょうか?

これを以下の部分均衡分析によって考察します

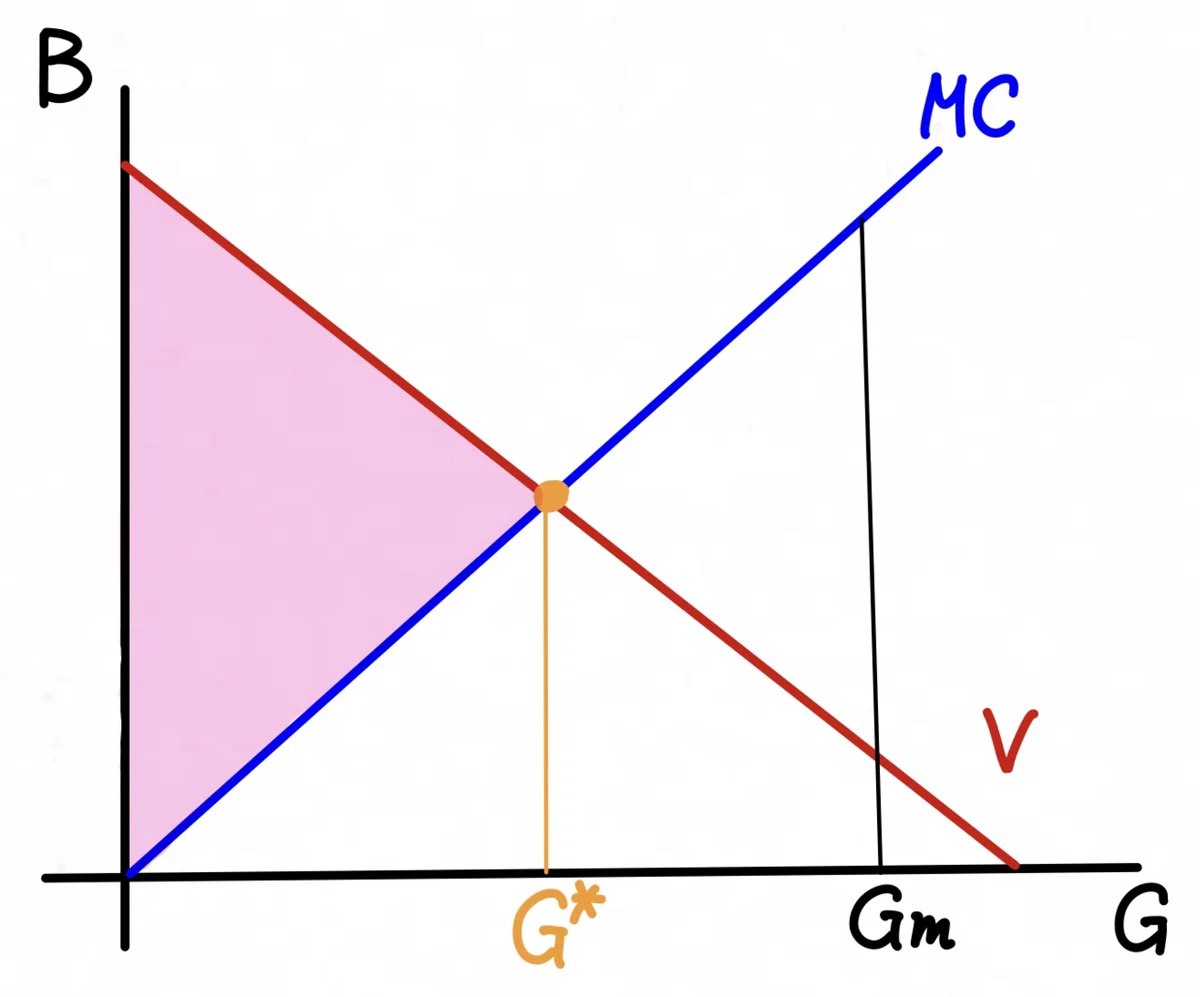

部分均衡分析:過剰か公共財供給

部分均衡分析:過剰か公共財供給

結論から述べると、予算額を最大にしようとして設計されたBmに対する公共財水準Gmは、社会的に望ましい公共財供給量とは言えません

なぜならば、部分均衡分析において社会的総余剰を最大化させていないからです

上記の図においてピンク色でハイライトした部分がこの経済の公共財市場における余剰になります

したがって、上図におけるG*が実現している

点で、社会的総余剰は最大化されていますから

G*の公共財供給量が、社会的に最も望ましいと言えるのです

これは、図解において予算を最大化するために供給された公共財供給量Gmが

社会的に望ましい公共財供給量であるG*と比較して「過剰に」供給されているということを示しているのです

これが、ニスカネン・モデルに基づく公共財供給の決定プロセスであり、予算編成過程における官僚の意志決定メカニズムを説明していると言えるのです

ニスカネン・モデルの発展的議論

ニスカネン・モデルを出発点として、官僚制に関するさまざまな理論的・実証的研究が展開されています👍

例えば、① 官僚の目的を修正した内容です

具体的には、予算の最大化以外の目的の導入するなど、モデルの発展を図っています

また、②生産の非効率(X非効率)という存在も考慮された研究が蓄積しています

ニスカネン・モデルの仮定において、公共財の供給のための生産は効率的に行われていると暗黙のうちに設定されていました

しかし、現実の社会はどうでしょうか?

生産の非効率性を考慮したら

予算編成過程における官僚の行動が変わってくるのかもしれません

実際には会計検査院の検査で明らかになっているように、多額の無駄な支出の存在が財政上における問題ともなっていますので

ニスカネン・モデルにおいて、社会的総余剰を最大化させる公共財供給量よりも予算を最大化させるために実現した公共財水準が「過剰」であることとの整合性はあると思いますね💖

本日の解説は、以上とします📝

ぜひ、これらの知見をベースとして

実際の世の中の経済動向に当てはめて考えていくという応用を効かせて

経済の仕組みを基礎的モデルから

ご理解されることを推奨いたします💗

関連記事のご紹介🔖

付録:私の卒論研究テーマについて🔖

私は「為替介入の実証分析」をテーマに

卒業論文を執筆しようと考えています📝

日本経済を考えたときに、為替レートによって

貿易取引や経常収支が変化したり

株や証券、債権といった金融資産の収益率が

変化したりと日本経済と為替レートとは

切っても切れない縁があるのです💝

(円💴だけに・・・)

経済ショックによって

為替レートが変化すると

その影響は私たちの生活に大きく影響します

だからこそ、為替レートの安定性を

担保するような為替介入はマクロ経済政策に

おいても非常に重要な意義を持っていると

推測しています

決して学部生が楽して執筆できる簡単なテーマを選択しているわけでは無いと信じています

ただ、この卒業論文をやり切ることが

私の学生生活の集大成となることは事実なので

最後までコツコツと取り組んで参ります🔥

今後も経済学理論集ならびに

社会課題に対する経済学的視点による説明など

有意義な内容を発信できるように努めてまいりますので、今後とも宜しくお願いします🥺

マガジンのご紹介🔔

こちらのマガジンにて

卒業論文執筆への軌跡

エッセンシャル経済学理論集、ならびに

国際経済学🌏の基礎理論をまとめています

今後、さらにコンテンツを拡充できるように努めて参りますので、今後とも何卒よろしくお願い申し上げます📚

最後までご愛読いただき誠に有難うございました!

あくまで、私の見解や思ったことを

まとめさせていただいてますが

その点に関しまして、ご了承ください🙏

この投稿をみてくださった方が

ほんの小さな事でも学びがあった!

考え方の引き出しが増えた!

読書から学べることが多い!

などなど、プラスの収穫があったのであれば

大変嬉しく思いますし、投稿作成の冥利に尽きます!!

お気軽にコメント、いいね「スキ」💖

そして、お差し支えなければ

フォロー&シェアをお願いしたいです👍

今後とも何卒よろしくお願いいたします!