Patricia and Christian talk to author and MMT scholar Phil Armstrong about inflation, hyperinflation, the gold standard, John Maynard Keynes’ Bancor plan and more.

Phil talks about the Ruhr Valley, the industrial region of Germany which was invaded and occupied by French and Belgian troops from 1921 to 1925 as a reprisal for Germany failing to fulfil World War I reparation payments. More here: https://en.wikipedia.org/wiki/Occupation_of_the_Ruhr

Phil talks about the ERM (European Exchange Rate Mechanism), which locked together the various currencies of what were to become the Eurozone member nations at fixed or semi-pegged exchange rates. More here: https://en.wikipedia.org/wiki/European_Exchange_Rate_Mechanism

Today we consider the current debate about whether we need to return to fixed exchange rates and create a new reserve currency for the World – which might even be a supra-national currency. In general terms the calls for these sort of reforms reflect a misunderstanding of how a modern currency operates and also the opportunities the fiat monetary system presents to a national government which desires to advance public purpose (full employment and price stability). The claims for this type of currency reform also reflect serious misunderstandings about trade and the financial flows which accompany trade. More worrying is that the fixed exchange rate call is becoming a cause celebre for progressive economists who see flexible exchange rates as somehow a cornerstone of a neo-liberal free market plot against prosperity. Talk about being misguided. So this blog introduces these issues – and will probably be the first of several on the topic.

On March 23, 2009 the Governor of the People’s Bank of China (its central bank) Zhou Xiaochuan released a statement – Reform the International Monetary System – which proposes to replace the USD as the reserve currency of the World and instead create “an international reserve currency that is disconnected from individual nations and is able to remain stable in the long run”.

A report in the Financial Times (March 24, 2009) about the People’s Bank of China governor’s statement suggested that it was “a clear sign that China, as the largest holder of US dollar financial assets, is concerned about the potential inflationary risk of the US Federal Reserve printing money”. China has around $USD2,000bn in foreign exchange reserves.

The basic proposition proposed by the Governor is that:

Theoretically, an international reserve currency should first be anchored to a stable benchmark and issued according to a clear set of rules, therefore to ensure orderly supply; second, its supply should be flexible enough to allow timely adjustment according to the changing demand; third, such adjustments should be disconnected from economic conditions and sovereign interests of any single country.

He eschews the use of the USD in this regard because it is like any “credit-based national” currency because it the issuing country is “constantly confronted with the dilemma between achieving their domestic monetary policy goals and meeting other countries’ demand for reserve currencies”. I suspect political motives in the statement – asserting a re-balancing of power bases – but the motivation is not the point.

So the US is cast as either not supplying enough liquidity to the international community who desire USD for reserves in an effort to control domestic inflation or, alternatively, providing too much liquidity when it aims to stimulate domestic demand.

The Governor casts back to the 1940s – when John Maynard Keynes proposed the concept of an international currency unit (ICU) which he called the Bancor – its value would be based on the “value of 30 representative commodities”. The Bretton Woods system of fixed exchange rates rejected the concept of an ICU but by 1969, the IMF introduced so-called special drawing rights (SDRs) which tried to fill the role of an international currency. He notes that the “role of the SDR has not been put into full play due to limitations on its allocation and the scope of its uses. However, it serves as the light in the tunnel for the reform of the international monetary system.”

Currently, the value of SDRs is based on a four currency basket – the US dollar, the Yen, the Euro and the Sterling. Mr Zhou wants to expand the role of SDRs and broaden the basket of currencies that give the SDRs their value.

The plan proposes to establish “a settlement system between the SDR and other currencies” so that they would become “a widely accepted means of payment in international trade and financial transactions” rather than being used in transactions between government and the IMF.

He wants countries to start creating financial assets denominated in SDRs to “increase its appeal”. From a modern monetary theory (MMT) this would amount to the imposition of a further voluntary constraint on government sovereignty – borrowing in SDR’s (which is tantamount to borrowing in a foreign currency) – and increasing the national government’s exposure to insolvency risk.

The plan would put the IMF at the centre of activity as countries would be required to entrust some of their reserves “to the centralized management of the IMF” and gradually phase out existing reserve currencies.

He claims that:

… A super-sovereign reserve currency not only eliminates the inherent risks of credit-based sovereign currency, but also makes it possible to manage global liquidity. A super-sovereign reserve currency managed by a global institution could be used to both create and control the global liquidity. And when a country’s currency is no longer used as the yardstick for global trade and as the benchmark for other currencies, the exchange rate policy of the country would be far more effective in adjusting economic imbalances. This will significantly reduce the risks of a future crisis and enhance crisis management capability.

This statement has received a lot of attention in the press lately and feeds the massive scare industry driven by the Austrian school and others who have been hankering for a return to a fixed exchange rate gold standard system, without understanding particularly what that means.

More worrying it that the agenda is also giving comfort to a growing progressive groundswell – driven by a sort of blind devotion to John Maynard Keynes – that a supra-national currency is desirable – and that the financial crisis has been a reflection of the failure of the flexible exchange rate system. It is very scary when heterodox economists get into bed with Austrians.

These scaremongers are pointing out that the recent fall in the USD parity and the huge public debt that the US Government has voluntarily accumulated as it increased its net spending to ward off another Great Depression ultimately will lead to a collapse in the international monetary system via inflation of the World’s reserve currency.

Domestic commentators in the US are suggesting the fall in the USD parity is a sign that inflation will emerge via rising import prices and that financial markets will start building into their trading plans further depreciations which become self-fulfilling prophecies – that is the amorphous hedge funds drive a run on the dollar which sees it ultimately collapse.

The low interest regime is also indicated as being part of the problem but once the run begins the central bank (the Fed) may not be able to set an interest rate high enough to quell the sell-off of the USD. Crisis then follows. This is the standard line used against deficit expansion in less developed countries and leads to the conservatives advocating the worst of everything – budget surpluses and increased starvation and dollarisation or exchange pegs.

If the USD becomes “worthless” because there are “too many of them flooding the markets” then the scaremongers claim that China will dump it (HOW?) and so the US government will lose its source of finance and will have to dramatically cut its deficit.

The worse case scenarios then suggest the US Government will become bankrupt and require IMF assistance. Pestilence then follows.

The other claim is that the once the Bretton Wood system collapsed the US government gained new policy ascendancy because it was no longer subject to the gold standard convertibility constraints. The argument then went that the US could live well beyond its means by selling USD-denominated debt without having to accumulate foreign reserves and periodically inflating the value of them away.

From a MMT perspective, we have dealt with all those myths before. The Chinese government does not issue USD so cannot possibly provide them to the US Government to spend. The US Government can always spend in USD as long as there are goods and services available for sale in that currency. Given that unemployment is above 10 per cent now, we know that there are millions of workers who would accept a public sector job with USD wages being the reward – so there are free resources that the US Government can purchase which are currently not being demanded by anyone else.

The US Government can never become bankrupt in terms of transactions made in US dollars. That is impossible unless they get a mad desire, for political reasons, to start defaulting on obligations denominated in their own currency. That is so far-fetched to be impossible.

Further if the Chinese Government decides to reduce its holdings of USD reservcs what are they going to do with them?

Short of dumping them in the sea they have to spend them and in this current parlous state of deficient aggregate demand that would both stimulate the US economy and reduce the US government’s budget deficit via the automatic stabilisers. US employment would likely rise and things would look better all round. Where is the problem?

Even progressives have suggested that the only “debt” solution for the US Government is to default or inflate its value away. For example, in an interview on the national broadcaster in Australia earlier this year, Steve Keen advocated that the Government should get rid off its debt by causing higher inflation or cancelling it and nationalising the banking system – he was quoted as such:

Ultimately, we’re going to see governments changing across either to abolishing debt, or to literally printing money rather than running out debt to finance their spending.

But the very existence of a current account deficit is a sign that foreigners desire to accumulate financial assets denominated in your currency. This applies to all countries. Once Bretton Woods collapsed all countries that issued their own currencies became sovereign in that sense. This was not confined to the US.

While it is true that the existence of the US dollar as a desired reserve currency means that they do not have to worry about foreign reserves as much as other nations with less attractive currencies, this doesn’t undermine domestic sovereignty.

Further, more and more progressives are suggesting the sort of financial reforms proposed by the Chinese central bank governor. For example, well-known “progressive” George Monbiot thinks he has the solution to the financial mess when he wrote how he would go about Clearing Up This Mess. He said:

… One of the reasons for financial crises is the imbalance of trade between nations. Countries accumulate debt partly as a result of sustaining a trade deficit. They can easily become trapped in a vicious spiral: the bigger their debt, the harder it is to generate a trade surplus. International debt wrecks people’s development, trashes the environment and threatens the global system with periodic crises.

As Keynes recognised, there is not much that the debtor nations can do. Only the countries which maintain a trade surplus have real agency, so it is they who must be obliged to change their policies. His solution was an ingenious system for persuading the creditor nations to spend their surplus money back into the economies of the debtor nations.

He proposed a global bank, which he called the International Clearing Union. The bank would issue its own currency – the bancor – which was exchangeable with national currencies at fixed rates of exchange. The bancor would become the unit of account between nations, which means it would be used to measure a country’s trade deficit or trade surplus …

First, some background for the non-economists.

Under the Bretton Woods fixed exchange rate agreement, there were two types of countries – those with external deficits and those with external surpluses. The former faced continual downward pressure on their exchange rate because the supply of their currency was always greater than the demand for it (via trade). As a consequence, the governments of these countries were forced to continually deflate their domestic economies, because monetary policy had to defend the exchange rate. Fiscal policy then had to be passive to avoid the stop-go growth patterns that were common.

The domestic deflation arises because the governments had to purchase the excess supply of currency in the foreign exchange markets to maintain a balance between supply and demand at the level appropriate to hit the agreed parity.

The first problem such a government faced was a shortage of foreign reserves which it required so that it could keep buying up its own currency in the foreign exchange markets. But the domestic impacts – the resulting stagnation (high unemployment) also created massive political problems for the governments.

Taken together the incentive then was to devalue the currency (which was permitted under the Bretton Woods system).

The problem then was that other countries became disadvantaged by the devaluation of one currency and the incentive then existed for what were called “competitive devaluations” – which in net terms were clearly counter-productive.

The point is that under the Bretton Woods system, all the adjustment pressure was on the external deficit countries because they faced continual currency collapse. There was clearly a disincentive for surplus countries (given they had conned their populations into believing shipping away more real goods and services than they received back via imports was a “good thing”) to increase their own imports and restore some balance in world trade.

Under the Bretton Woods system, the surplus countries also stockpiled foreign currency reserves which insulated them from any currency crises and their central banks would sterilise the domestic impacts of the net exports boom by issuing bonds (to drain the domestic currency expansion that was occuring in the foreign exchange markets as the government kept the parity from rising).

Taken together these tensions were unsustainable and that is why the fixed exchange rate system collapsed in 1971. The clear aim of Keynes’s plan was to stabilise exchange parities by redistributing the adjustment burdon when trade imbalances arose.

How would this work? How would an international currency unit operate? The original proposal from Keynes was that the Bancor – tthe new currency unit – would have its value fixed to 30 commodities including the price of gold. The justification advanced at the time was that using a broad basket of commodities to peg the Bancor would stabilise its movements (averages of many are less volatile than a peg to one).

Any country which signed up to the newly-created International Clearing Union (ICU) would have bancor account and an overdraft facility. At the outset, the ICU would allocate bancors to each country in proportion to their trade volumes (exports and imports). The bancors would not be convertible back into gold and so would become the reserve currency.

A deficit nation would be penalised if its overdraft reached 50 per cent of its allowance. If the problem persisted then it would eventually have to devalue to head off any capital flight.

But surplus nations would lose their stock of bancors above the overdraft limit at the end of each year which would force them to shed the accumulation – presumably by increasing their demand for imports. More modern versions of the scheme suggest that a nation could provide international aid as a way of expending the surplus bancors.

The essential point is that both deficit and surplus nations would have to make adjustments in goods and services flows.

But note this is all about goods and services trading against goods and services. There is clearly separate movements in financial assets. For example, a determined speculative attack would destroy the peg very quickly just as they can undermine a flexible exchange rate. The bancor system will not improve things in this case. And it is largely these financial flows which we consider to be the dangers in a flexible exchange rate system.

History however tells us that the system was not adopted and instead Bretton Woods was introduced with the IMF becoming the main international agency and subsequently managing the SDRs.

That system has not worked well. Monbiot is interesting here:

The consequences, especially for the poorest indebted countries, have been catastrophic. Acting on behalf of the rich world, imposing conditions which no free country would tolerate, the IMF has bled them dry. As Joseph Stiglitz has shown, the Fund compounds existing economic crises and creates crises where none existed before. It has destabilised exchange rates, exacerbated balance of payments problems, forced countries into debt and recession, wrecked public services and destroyed the jobs and incomes of tens of millions of people.

The countries the Fund instructs must place the control of inflation ahead of other economic objectives; immediately remove their barriers to trade and the flow of capital; liberalise their banking systems; reduce government spending on everything except debt repayments; and privatise the assets which can be sold to foreign investors. These happen to be the policies which best suit predatory financial speculators(8). They have exacerbated almost every crisis the IMF has attempted to solve.

This is why we should abandon this approach where the IMF is the international bully imposing harsh “fixed exchange rate” regimes on poor countries. The IMF or a replacement (clearing out all the senior executives to refresh the organisational culture) should instead serve a role to counter-balance speculative attacks. All nations might deposit volumes of their currencies at this organisation which it would then use, under the instruction of the national government facing an external currency issue, to stop a currency free-fall.

I am developing this idea further at present. This blog partly covers these issues and options – Current accounts and currencies.

So what is wrong with the bancor idea? Well it remains a fixed exchange rate system.

Any country that pegs its currency to a foreign currency (or unit that it doesn’t issue under monopoly conditions) immediately imposes constraints on both fiscal and monetary policy which are not present under flexible exchange rates.

When a government promises to convert its currency into another currency (or unit) at some fixed rate, then it always has to hold enough reserves of that currency (or unit) to satisfy all demands for such conversions. We could conceive situations where the reserves required to be held could be huge and at least equal to the outstanding domestic high powered money and public debt.

It is easy to see how budget deficits then become problematic to the fixed parity for nations that do not enjoy large current account surpluses (which add to foreign reserves). An expansionary domestic policy position may stimulate imports which then invoke downward pressure on the exchange rate and the loss of reserves. Fiscal policy thus becomes subjugated to the need to maintain a fixed (agreed) external parity.

Similarly, under flexible exchange rates, the central bank sets the interest rate – that is, it is exogenous – and under the control of the government (using government to mean the consolidated treasury/central bank). Under fixed exchange rates, this capacity is also lost and the interest rate become endogenous – which means it must be adjusted to defend the external parity.

So, as noted above, when there is a current account deficit, interest rates have to rise and vice-versa. This is because higher interest rates are thought to attract financial capital inflows which help maintain foreign reserves.

The other point to note is that monetary and fiscal policy work against each other with both being constrained by the fixed exchange rate arrangement. So it follows that a rising budget deficit will drive interest rates up – both because the government spending competes with private spending for funding (only in a convertible currency system) and because the central bank has to defend the exchange parity to ensure the nation doesn’t exhaust its holdings of foreign reserves.

So it is important to realise that most of the analysis of fiscal and monetary policy that you read in newspapers and hear in the spoken media is based on the policy constraints that arise under fixed exchange rates.

But when we have flexible exchange rates, the playing field changes dramatically. There is no government budget constraint – it moves from being a a priori financial constraint to being an ex post accounting identity, with little interest to anyone other than accountants.

As a result, governments do not have to raise funds in order to spend but just credits bank accounts and thus adds to bank reserves. The two tools thought to be “financing” spending – taxation and debt-issuance – do nothing of the sort. As I discussed in this blog – Functional finance and modern monetary theory – taxation and bond-issuance are policy tools that allow the government to change the non-government sector holdings of purchasing power and/or changes the composition of assets it holds.

Taxation drains reserves (destroys financial assets) as the reverse of government spending adding to reserves (creating financial assets). A budget deficit thus creates net financial assets and a surplus destroys net financial assets.

The other important point is that because the fiat monetary system in a flexible exchange rate is not based on any convertibility of the currency (to some foreign currency or other commodity), the government can always add domestic reserves to the banking system in the currency of issue.

The lack of convertibility means that you get a $ coin back if you present a $ coin to the central bank and ask the government to honour its liability. But the essential point is that there is never a constraint on the government’s ability to add to bank reserves.

As a result, the interest rate becomes exogenous – bond issues/purchases are used to ensure there are just enough bank reserves on any particular day to allow the central bank to hit its target interest rate. So there is a clear break under a flexible exchange rate between budget deficits and interest rates that is not enjoyed under any form of fixed exchange rates.

Taken together, flexible exchange rates, far from being a free market plot, actually empower government’s domestic policy charter. With no link between interest rates and deficits then monetary policy and fiscal policy can function in a sympathetic (reinforcing) manner rather than being operating in an antagonistic manner.

Domestic policy targets (such as full employment) can thus be pursued more effectively with less external constraints. This is not to say that the external sector becomes dislocated by the domestic policy settings. A bouyant economy driven by domestic policy rather than net exports will probably put downward pressure on the exchange rate. Governments might handle this is various ways – they might run higher than otherwise interest rates or they might keep unemployment high.

But they might also let the exchange rate reach a new lower level which reinforces the competitiveness of its external sector and provides investment opportunities for foreign interests.

The point is that they government has choices which are absent in a fixed exchange rate system where monetary policy has to target the maintenance of the parity.

We may need additional policy tools to prevent the destruction of a currency by speculative attacks. The role for the IMF specified above would be one way to improve things. We might consider making certain trading modalities illegal (for example, along the lines of the bans on opaque short selling that many countries imposed at the height of the crisis). We might consider capital controls along the lines of Malaysia in the 1997 crisis. You will find some further ideas here – Operational design arising from modern monetary theory and Asset bubbles and the conduct of banks

I don’t advocate these as a matter of course but we should at all times consider alternatives adjustment mechanisms to the neo-liberal (IMF) domestic austerity campaign – that only damage the most disadvantaged.

A supranational currency – in general

Within this same debate, there are also some people who want to develop a pure supranational currency. That is the “bancor” would go beyond being a settlement unit for trade and be used by all people everywhere for all transactions.

While I was in Kazakhstan last week, I was invited to review the latest plan proposed by their president Nursultan Nazaybayev. He considers five different ways out of the crisis which he considers is the result of a “deficiency of the world reserve currencies.” His preferred solution which he calls the “Fifth Way” is the creation of a “supranational settlement-payment unit (and then of the currency) of a fundamentally new class”.

The plan is to create a new world currency which is not under the control of any particular country – so not unlike the Bancor – but the national currencies would disappear too.

When considering how this might be created the proposal says that we would need a “single organization, which will accomplish this task stepwise and practically.”

So while the Bancor-system imposes massive organisational and trust issues, the idea of a surpranational single currency means the following.

First, there would be one world central bank. This means that there would be one world short-term interest rate and therefore one world yield curve. I do not consider that is a viable organisational possibility. I also do not think there is sufficient homogeneity across our national spaces to make it desirable to have only one monetary policy. I do not need to outline all the obvious questions – where would the central bank operate from? who would elect the board? would it just be an IMF-type organisation which has failed the less developing nations so badly? etc.

Second, to avoid the dislocations that cripple the Euro, a single central bank has to be matched with a single treasury (running fiscal policy). So one world government unless we are going to allow macroeconomic policy to be conducted by a non-elected body like the IMF. That would be a disaster (see next point).

Third, by implication we would have only one world electorate. I don’t think much of the term democracy (given the control over the electoral process of the power elites) but it still transpires that in Australia we get to throw out our national government every three years if we dislike what they are doing. A change of government doesn’t necessarily improve things but it remains true that we can change our governments and force them – with some difficulty in certain situations – to obey the rule of law. I don’t think that “freedom” applies throughout the world to allow a unified electorate which can discipline the fiscal process via the ballot box.

Conclusion

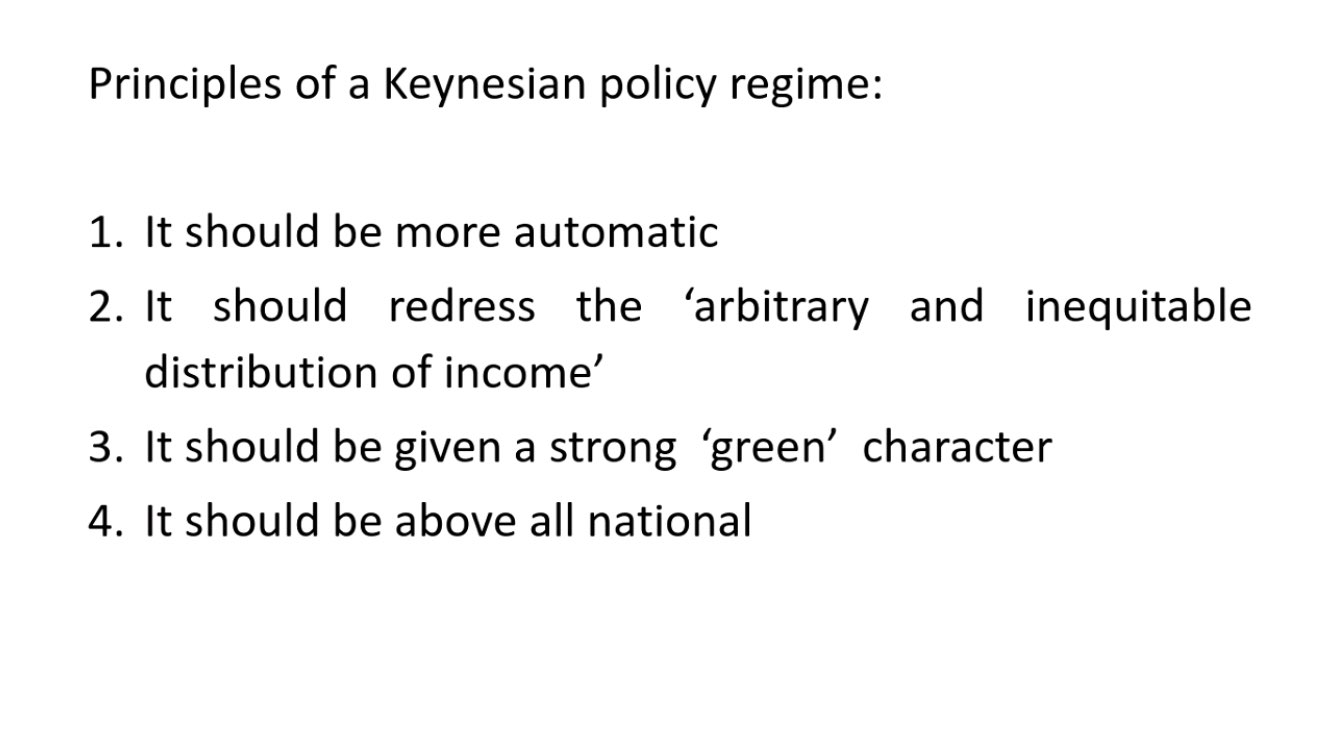

While I will write more about this in the future the solution to the financial instability that has brought the real production systems in our nations to their knees is not to surrender national currency sovereignty. The capacity of a national government to issue its own currency under monopoly conditions should not be surrendered to maintain an exchange rate system which is incapable of sustaining full employment across all sovereign spaces.

While the ICU plan was designed to overcome the forced deflationary forces which an external deficit it actually cannot do that without considerable loss of sovereignty. Unless you could have one treasury and one central bank then national units are always forced to sacrifice domestic policy to maintain the value of its currency against the supra-national settlement unit.

The political point is also not to be understated. Why should a sovereign national government (and its citizens) allow an international body (which might be unelected – in the case of the IMF) to implement policy that will affect its electoral appeal?

It is bad enough that we allow central bank boards who are unelected to motivate the direction of interest rates. It would be unthinkable to devolve the total fiscal and monetary authority to a supra-national body.

The other point is that the idea of a fixed exchange rate is rather illusory – speculative flows can break the peg very quickly anyway. Only countries such as China with enormous stockpiles of foreign reserves can resist these speculative attacks and run a peg against say the US dollar. But remember they have been able to build that stockpile by denying its citizens access to resources and thus keeping them poorer than they would otherwise have to be.

Finally, a deficit nation under a Bancor will still face deflationary prospects to maintain the value of its currency against the Bancor. No real change there.

In 1936 Keynes said that if democracies fail to tackle mass unemployment and inequality people would turn to dictatorship. It happened then and It's starting to happen now. It's time for a Second Coming of Keynesian social democracy. Here's my speech:

0 件のコメント:

コメントを投稿